iShares MSCI Russia ETF (ERUS)

Key Statistics

Thank you for reading this post, don't forget to subscribe!Daily Close 37.32 Long-Term Trend (100 SMA) Bullish

Minor Support Level 33.51 Minor Resistance Level 38.71

Major Support Level 19.64 Major Resistance Level 59.22

Minor Buy Signal 39.23 Minor Sell Signal 33.07

Major Buy Signal 62.08 Major Sell Signal 18.10

BRIEF OVERVIEW – Russia ETF

Certainly, not many people in the United States are big fans of Vladimir Putin. However, Putin has succeeded in resurrecting the Russian economy over the course of the past two decades. The entire economic system was in shambles when Putin became President of Russia in December 1999. He has slowly turned Russia into a major economic powerhouse on the global stage.

The majority of Russia’s economic success hinges on the commodity markets. Russia is a leading producer of crude oil, natural gas, wheat, gold, diamonds, timber and coal. In fact, over 30% of the world’s natural resources are located in Russia. Additionally, Russia has more than 20% of the world’s forests, making it the largest forest country in the world.

In terms of financial stability, Russia has one of the lowest debt-to-GDP ratios in the world. The current ratio is 12.9%, well below the United States @ 106.4%. During the past five years, Russia has substantially increased its gold reserves. It is now the fifth largest holder of gold. In addition to its low debt and large gold holdings, Russia’s currency (the Ruble) is becoming an important part of the global foreign exchange network. The demand for Rubles is slowly increasing as the country becomes a major player in the global economy.

The iShares family of exchange traded funds introduced the MSCI Russia ETF using the ticker symbol ERUS. The ETF was launched on November 9, 2010. ERUS provides broad exposure to several of the largest companies traded on the Moscow Exchange, Russia’s premier stock exchange. ERUS is the most heavily traded ETF devoted to the Russian economy.

SHORT-TERM VIEW – Russia ETF

ERUS has generated a sharp rally during the past eight months. The ETF has rallied approximately 40% since June 2017. Despite the brutal decline in the stock market a few weeks ago, the short-term momentum remains bullish. The next resistance level is 38.71. The bears need a weekly close below 33.51 to turn the momentum in their favor.

Based on the Aroon Oscillator, ERUS has a moderately overbought reading of +40. The Aroon Oscillator is programmed differently than most stochastic indicators. The oscillator fluctuates between -100 and +100. A reading of 0 would indicate a neutral position. Therefore, a reading of +40 with ERUS is considered moderately overbought. Most likely, the ETF is fairly close to a short-term top.

LONG-TERM VIEW – Russia ETF

Two decades ago, the Russian economy was left for dead as the country was attempting to transition from a controlled economy to a market based economy. Boris Yelstin was chosen to lead the country into a new economic frontier. Of course, these major economic transitions never go smoothly.

Following the collapse of the Soviet Union in 1991, a new Russian Federation was formed under Yelstin’s leadership. The main objective of the new government was to create macroeconomic stabilization along with economic restructuring. Yelstin implemented several fiscal and monetary policies designed to promote economic growth and stable prices. Specifically, the Russian government established a new banking system and allowed its citizens to own private property and start new businesses. Additionally, Russia opened its domestic markets to foreign trade and investment. This linked the Russian economy with the rest of the world, which was critically important to becoming part of the global financial system.

Throughout the 1990s, the Russian economy failed to gain momentum as it was struggling to embrace its new free enterprise system. Specifically, the country was unable to control its rate of inflation. As part of Russia’s plan to become a market based economy, the country removed all price control mechanisms in the early 1990s. Unfortunately, the appropriate technological and monetary infrastructure was not in place to handle such a dramatic change. Consequently, Russia suffered extreme levels of inflation throughout the 1990s. The average rate of inflation was well over 200% per year during this period of time.

In addition to hyperinflation, Russia’s currency (the Ruble) was experiencing dramatic fluctuations against other European currencies. As a result, Russia found it difficult to develop trade relations with other countries. Many potential trading partners would not accept the Ruble as a method of payment. Therefore, Russia had to find alternative payment methods in order to conduct business.

In an attempt to garner economic support from other countries, the new Russian Federation accepted the responsibility of settling all external debts from the old Soviet Union. On the surface, this was viewed as a step in the right direction for the newly established country. However, it placed additional stress on the economy.

Although the new Russian Federation did manage to improve its standing on the global stage during the 1990s, the improvement was modest and extremely erratic. Boris Yelstin resigned as President in December 1999. Vladimir Putin officially became Acting President of the new Russian Federation on December 31, 1999. He easily won the subsequent 2000 presidential election by a wide margin.

Upon taking office, Putin immediately went to work on improving the economy along with strengthening Russia’s trade relations with other countries. Putin’s new policies were extremely effective in reviving the Russian economy. The Russian economy expanded for eight consecutive years, as Putin concentrated on leveraging the country’s abundant supply of natural resources. In fact, over 30% of the world’s natural resources are located in Russia. Additionally, Russia has more than 20% of the world’s forests, making it the largest forest country in the world. Within the first five years under Putin’s leadership, Russia became a leading producer of crude oil, natural gas, wheat, gold, diamonds, timber and coal.

Admittedly, much of Putin’s initial success in the early 2000s can be attributed to pure luck. Putin took office just as the commodity universe was about to unleash one of its greatest bull markets of the past 100 years. Putin was able to ride the wave of the commodity bull market by establishing trade agreements with several G20 countries.

Today, the Russian economy continues to power forward. However, there have been periods of weakness, particularly following the financial crisis of 2008 along with a commodity bear market beginning in 2011. However, the economy is in much better shape today versus 20 years ago. In fact, Russia is enjoying is lowest level of inflation since the country began tracking economic numbers beginning in 1991. The current inflation rate is 2.2%

It certainly appears the Russian economy is in the early stages of generating a renewed burst of economic activity, which could easily last for the next 5 to 10 years. The catalyst for economic growth will be driven by a new commodity bull market.

The commodity universe is still in a secular bull market, which began in 2001. However, commodities have been in a cyclical bear market since 2011. Most likely, the cyclical bear market ended in 2016. If the cycle data is correct, commodity prices are poised to move higher for the next five years (maybe longer). This new cyclical commodity bull market could be extremely powerful because overall commodity prices at near an all-time historic low in relation to other asset classes.

Based on current economic trends and commodity cycles, the Russian economy is in a perfect position to enjoy a sustainable period of strong growth. Everything appears to be lining up in Russia’s favor.

Despite a powerful advance during the past two years, ERUS remains in bearish territory from a long-term perspective. The bulls need a weekly close above 59.22 in order to capture the bullish momentum. A powerful commodity bull market during the next five years could easily propel ERUS above 59.22. However, it won’t happen any time in the near future.

SHORT-TERM CHART – Russia ETF

Please review the 6-month chart of ERUS. The short-term chart pattern remains bullish. ERUS produced an impressive recovery following the brutal stock market decline a few weeks ago. The ETF continues to make higher highs, which is very bullish. The next resistance level is 38.71. The chart pattern will turn bearish on a weekly close below 33.51.

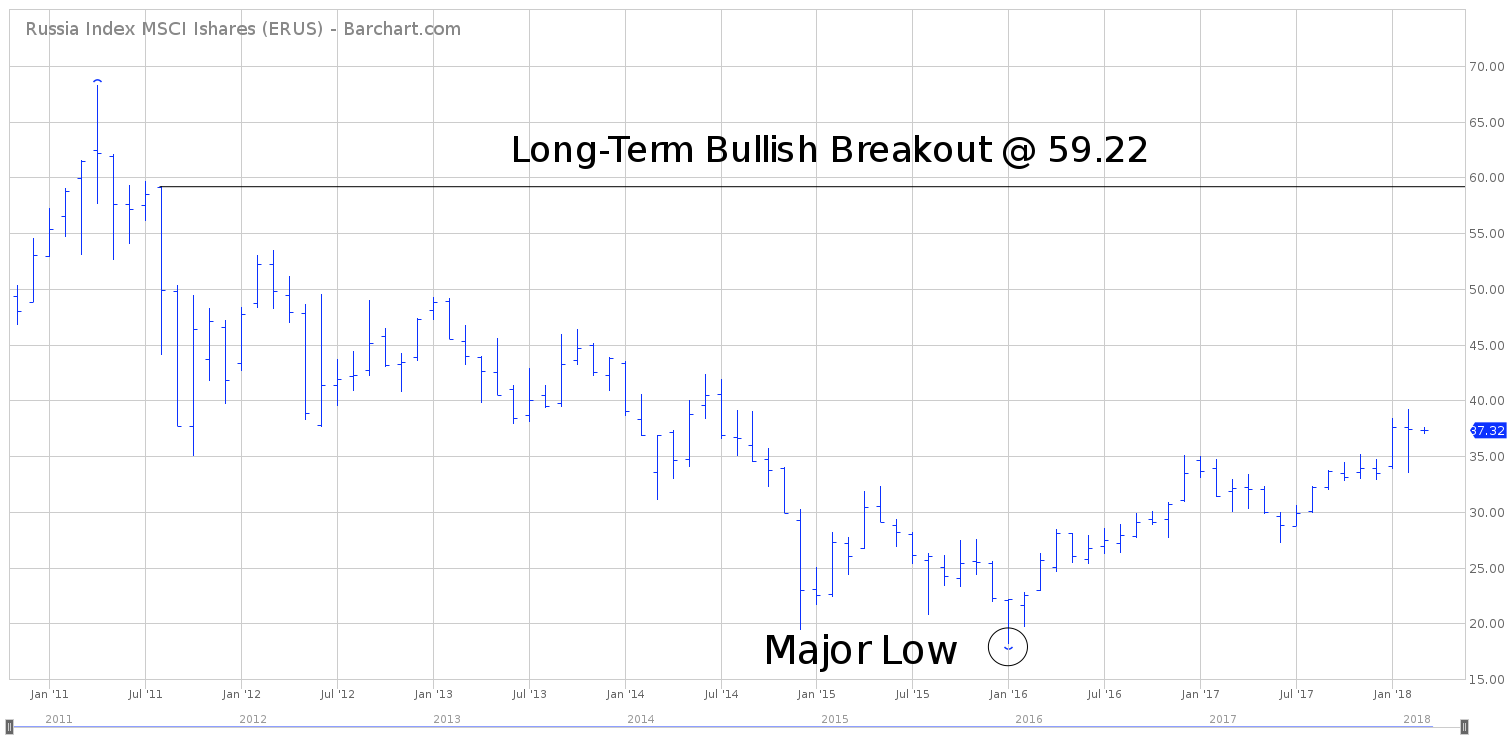

LONG-TERM CHART – Russia ETF

Please review the 8-year chart of ERUS. This chart covers the entire trading history of the ETF. ERUS has enjoyed a strong rally during the past two years. However, the long-term chart pattern is still bearish. Based on the chart formation, it certainly appears ERUS formed an important bottom in January 2016, @ 18.10. The chart will turn bullish on a weekly close above 59.22.